{kind=link}

Rubin, T. and Panaretos, V.M. (2020). Spectral Simulation of Functional Time Series. arXiv:2007.08458

Software: R package ‘specsimfts’

Nontechnical description:

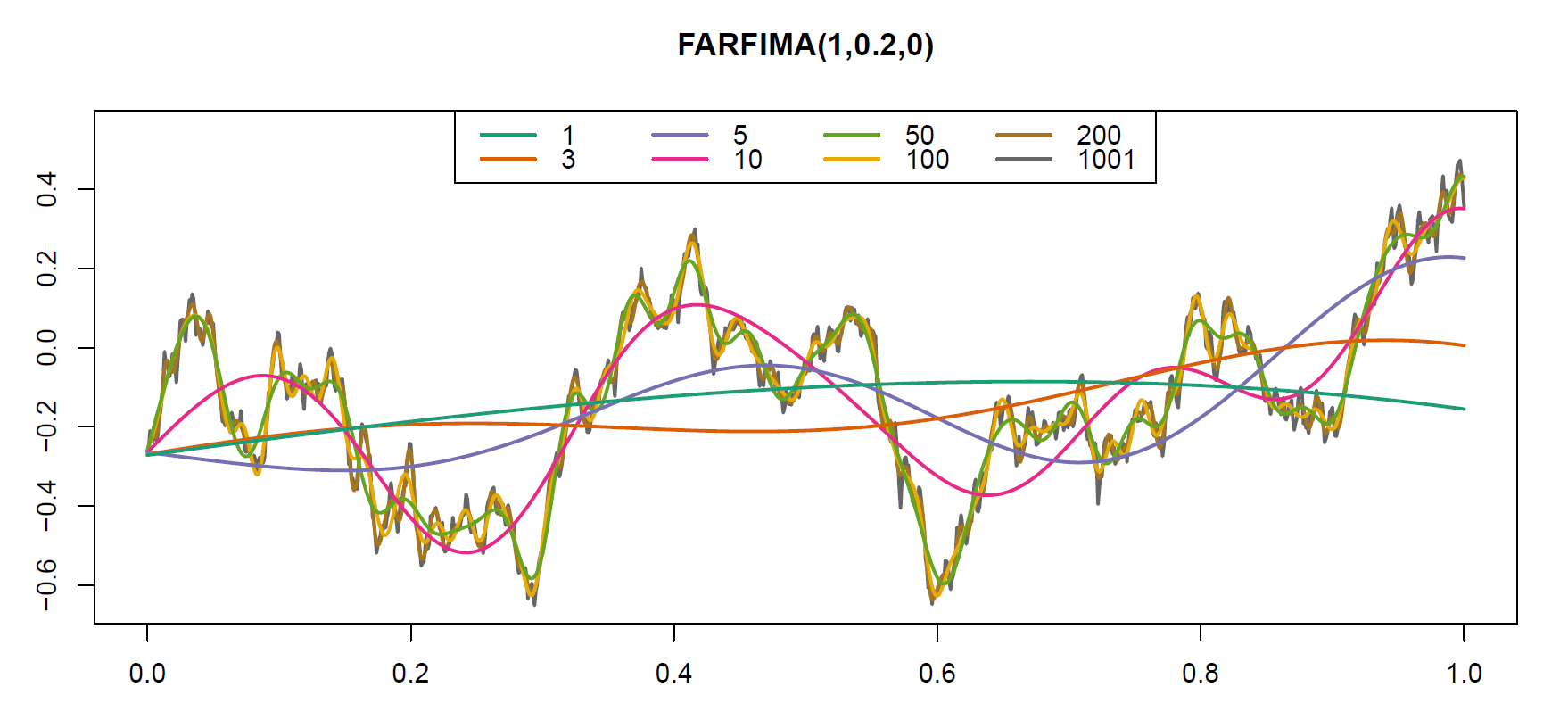

- In this paper I developed a simulation method for generating samples of functional time series. The simulation of the signal is performed in the so-called spectral domain where some dynamics aspects become simpler and thus the method allows for simulation of such processes for wich no other alternative existed before. Moreover the simulation by my method can be up to 100x faster, in some cases, compared to the previous simulation methods.

- The accompanying R-package ‘specsimfts’ can become a useful tool for researchers in functional time series wanting to probe the performance of their statistical methods by reducing their time spend on implementing simulation studies.

- As a secondary contribution the paper provides with some theoretical results on spectral analysis on some functional time series.

Abstract:

We develop methodology allowing to simulate a stationary functional time series defined by means of its spectral density operators. Our framework is general, in that it encompasses any such stationary functional time series, whether linear or not. The methodology manifests particularly significant computational gains if the spectral density operators are specified by means of their eigendecomposition or as a filtering of white noise. In the special case of linear processes, we determine the analytical expressions for the spectral density operators of functional autoregressive (fractionally integrated) moving average processes, and leverage these as part of our spectral approach, leading to substantial improvements over time-domain simulation methods in some cases. The methods are implemented as an R package (specsimfts) accompanied by several demo files that are easy to modify and can be easily used by researchers aiming to probe the finite-sample performance of their functional time series methodology by means of simulation.